Today we have a special report from Tim Price – Director PFP Wealth Management and Scott Campbell – Fund Manager MitonOptimal.

Valuation Vs The Momentum Trade

Scott Campbell, Managing Director and Fund Manager

Many multitudes of commentators are pointing out the blinding glimpse of the obvious. “Would you prefer a regular income likely to rise at least as fast as inflation or a lower fixed income with no prospect of increases?” Many dividend yields on blue chip global companies now offer a higher income yield than government bonds in the US, UK, Europe and Japan. Historically high dividend yields vs 10 year Government Bond yields is a buying opportunity for stocks, particularly in deflationary Japan. P/E multiples are at levels not seen for a generation, free cash flow is fantastic and balance sheets are great. Recent M&A shows that CEO’s think there is value plus value, fund managers are jumping out of their skin! The valuation argument is equally as compelling as it was in 2008/09.

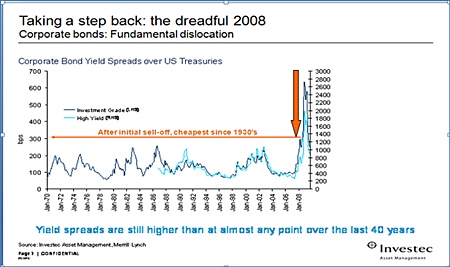

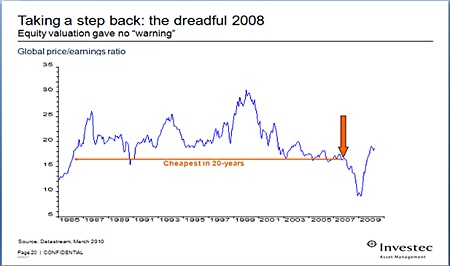

The following two charts from Investec show how in June 2008 corporate bonds and equities were then at valuation levels considered cheap. They then proceeded to fall 30% or more! In fact Government Bond yields were at 30 year highs in June 2008; i.e., the most expensive for three decades, and then proceeded to go higher!

Clearly values are much better in developed world equities after indices have gone nowhere for 10 years. However, economic fundamentals are not looking good for the rest of the year. As 1999 or 2008 showed, valuation alone is not a great predictor of short term movement either way and the market can remain irrational longer than you can remain solvent.

Die Hard, with a vengeance

Tim Price, Director of Investment PFP Wealth Management

“Money is like manure. You have to spread it around or it smells.” – J. Paul Getty.

When it comes to dying hard, the cult of equities has few peers. You might have thought that the dot.com bust, the Enron / Worldcom scandals, the recent cascade of banking crises and the current widening stagflation would have beaten equity investors into some kind of sense of submission or at least acceptance by now. Not a bit of it.

Notwithstanding the fact that global equity markets, as defined by the MSCI World Equity Index, are currently 22% below their level at the start of 2000, let alone a third below their highs of Q3 2007, the investment media continue breathlessly to report their every move.

One can only conclude either that the modern equity investor is a glutton for punishment, or that the modern media producer is a sadist. The average radio or TV business report, if it offers any coverage of markets whatsoever, will tend to focus exclusively on the performance of equity indices. Even interest rates, for example, barely get a look in.

Open a typical newspaper, journal or even financial magazine, and see how much coverage – if any – is given to any other asset class than common stocks. For that matter, consider how much focus the fund management industry (retail or institutional) places upon equity vehicles as opposed to any other.

While many funds may be launched whereas few will ultimately be chosen, it represents a real triumph of marketing over relevance to continue to peddle products that few consumers are likely to need, let alone want. The financial services industry surely attained critical mass by way of long-only equity variety years ago – and the growth of exchange-traded funds has not exactly diminished choice.

It is testimony to the lingering attraction of the equity myth that it continues to this day to drive the production of redundant product by an endless array of me-too providers. Of course not all funds are bad, and not all equity funds are bad; but the signal to noise ratio, given the population of the managed fund universe, has to be low. Most critically, in the context of managed funds, know what you own – which will take some of the sting out of any exposure to managed equities in the context of a potential bear market.

To be continued…

The above data and research was compiled from sources believed to be reliable. However, neither MBMG International Ltd nor its officers can accept any liability for any errors or omissions in the above article nor bear any responsibility for any losses achieved as a result of any actions taken or not taken as a consequence of reading the above article. For more information please contact Graham Macdonald on [email protected]

{kind=link}