Back in March, Russia’s authorisation of its armed forces to be used in Ukraine brought about widespread condemnation, particularly from the EU1 and the US2.

Before the Crimean crisis broke out, Russia had become popular with emerging markets investors: one of the BRIC countries with Brazil, India and China. For example, by December 2013, US financial institutions had put over USD 37 bn into the country, which, according to eVestment, was almost double the amount of just three years previously.3

Investors walk away

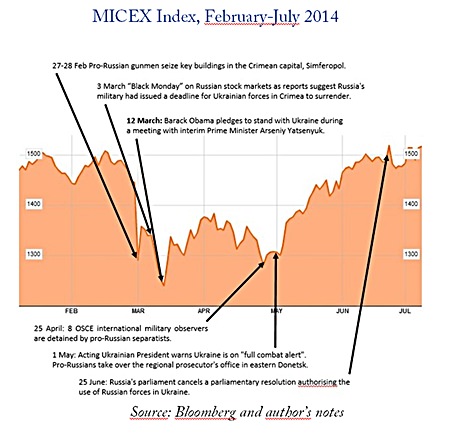

Then, Russia swiftly annexed Crimea following political unrest in Ukraine. International investors reduced exposure to the Russian stock market driving the MSCI Russia Index to a low of -25% in mid-March.4 At the end of March, the stock exchange’s market cap was around USD 430 bn – less than that of Apple alone.5

Shockwaves of the crisis were also felt in Eastern Europe as a whole: outflows of USD 2.4 bn in 2013 were followed by withdrawals of USD 1 bn between the beginning of January and end of March this year. Added to that, dozens of other broader emerging markets funds with exposure to Russian stocks also experienced redemptions.6

After a brief recovery, the news that OSCE observers were seized in the Ukraine and the US imposed sanctions on Russian President Vladimir Putin’s inner circle, was followed by another significant drop in the stock market in late April.

A bad risk for some, an opportunity for others

Yet, like a good magic trick, a political crisis can deflect focus from the seemingly obvious. With international investors walking away, prices in Russian equities reduced sharply. Of course, no-one could really predict the economic effects of the situation in Crimea and Eastern Ukraine. However, those with a long-term approach to investment recognised a good opportunity to invest in Russia, holding the belief that the crisis would not last forever and values would at some point rise again. I suggested this on CNBC in the early days of the crisis7.

Political stability

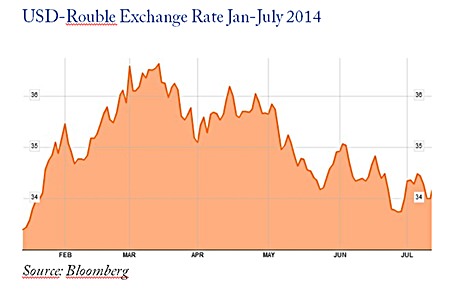

By summer 2014, the political sabre-rattling had calmed down somewhat and the pro-Russia militia’s occupation of Eastern Ukraine had ended. Meanwhile, stock prices and the USD-rouble rate had both gone back up to their pre-crisis levels.

These indicators show that those with a longer-term attitude towards Russia and bought in while the markets were cheaper may have got themselves a bargain. After all, there is far more to a country’s economy than its politics, as any investor in Thailand or Italy would confirm.

Russia is the largest country in the world and has significant resources. In May of this year the government signed a 30-year USD 400 bn gas-export contract with China8. Added to that, President Putin recently approved a government stimulus package which includes: simplifying procedures for granting state guarantees; tax exemptions for new companies; increased spending on infrastructure; plans to promote industry and agriculture; and amendments to improve deductibility of taxes and fees.

Analysis of the fundamentals is key

Although the political situation was still uncertain when Standard & Poor’s published its last ratings report on Russia at the end of March,9 it expected that the rouble would stabilize at March levels and that capital outflows would slow to a modest pace. This seems to be the case, as the Russian central bank announced in late May that it estimated capital outflows would be between USD 85 bn and USD 90 bn; which is much better than the foreign minister’s fears that USD 160 bn would leave the country in 2014.10

Looking at the stock market patterns over the last three years, the Ukraine crisis seems to have taken a similar shape to that of three other confidence dips since 2011, which have all resulted in stabilisation around previous rates.

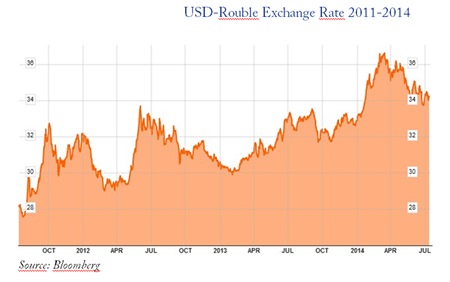

The US dollar-rouble rate shows a strengthening of the rouble; however, it is still much weaker than rates at the turn of the year. That said, the Russian currency had been weakening against the dollar since February 2013, from 30 to over 36 RUB : 1 USD in mid-March 2014. Thus, the Ukraine situation merely exaggerated a trend that was already present.

Taking all the above into consideration, it is apparent that certain countries experiencing a political crisis can actually represent good value in the medium-to-long term. When considering investment, a mere glimpse of a news bulletin is of course not enough. Instead, independent analysis from a variety of sources covering the short, medium and long term is far more helpful. After all, whatever may be happening on our television screens, the economic fundamentals are still in place, the country could well bounce back in a matter of months.

Footnotes:

1 http://consilium.europa.eu/homepage/showfocus?focusName=ukraine-eu-condemns-russias-actions%2C-calls-for-de-escalation-and-remains-ready-for-further-measures&lang=en

2 http://www.reuters.com/article/2014/03/02/us-ukraine-crisis-usa-kerry-idUSBREA210DG20140302

3 http://fortune.com/2014/03/31/time-to-invest-in-russia/

4 http://www.fmgfunds.com/index.php/contact-en/337-russian-highlights

5 http://fortune.com/2014/03/31/time-to-invest-in-russia/

6 http://www.ft.com/intl/cms/s/0/9e3e6dd2-b4df-11e3-9166-00144feabdc0.html#axzz37ACwwOHU

7 http://video.cnbc.com/gallery/?video=3000249455

8 http://www.fmgfunds.com/index.php/component/content/article/3-news-en/337-russian-highlights

9 http://www.standardandpoors.com/spf/upload/Events_US/4214_art3.pdf

10 http://www.telegraph.co.uk/finance/economics/10851844/Russias-central-bank-chief-deems-crisis-over-as-capital-flight-is-halted.html

| Please Note: While every effort has been made to ensure that the information contained herein is correct, MBMG Group cannot be held responsible for any errors that may occur. The views of the contributors may not necessarily reflect the house view of MBMG Group. Views and opinions expressed herein may change with market conditions and should not be used in isolation. MBMG Group is an advisory firm that assists expatriates and locals within the South East Asia Region with services ranging from Investment Advisory, Personal Advisory, Tax Advisory, Private Equity Services, Corporate Services, Insurance Services, Accounting & Auditing Services, Legal Services, Estate Planning and Property Solutions. For more information: Tel: +66 2665 2536; e-mail: [email protected]; Linkedin: MBMG Group; Twitter: @MBMGIntl; Facebook: /MBMGGroup |

{kind=link}