One of the factors that has eased the pain of sending money back to Australia lately has been the strength of the Thai Baht. Thai residents earning in local currency have suffered nowhere nearly as badly as those paid in US Dollars (USD) or (God forbid) in Sterling. However, the sustained rebound in the Australian Dollar (AUD), which started in 2008, may well be coming to an end and that could bring with it a whole raft of both risks and opportunities.

Admittedly, I have been calling the end of the latest AUD spike since the end of 2011. Yet, when currencies form a top or a bottom it is frequently a process rather than an event.

Before I look at the AUD itself, I will take a slight detour into risk management. The worst time to have exposure to a stock is when a company is in trouble. If that company stock is in your pension as well as your investment account, the problems are even worse. Added to that, if that company is your employer and because of its problems lays you off, disrupting your earnings and rendering all your stock options worthless, then you are really up against it.

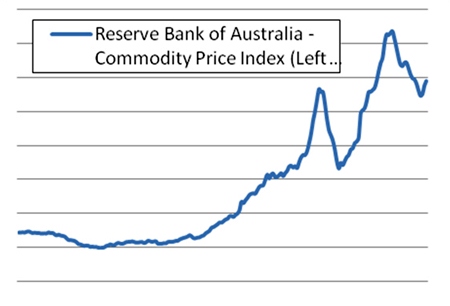

AUD Exchange Rate (vs. USD) and Commodity Prices

I would not suggest to people that they should not invest in their employer’s stock or hold it in their Super plan but I would ask them to be aware of the risk. Similarly, there may be risks related to any weakening of the AUD – what if your employer pays you here in Bangkok in AUD? Your employer would benefit from that but life in Bangkok will suddenly get much more expensive overnight for you. On the other hand, if you are paid in Baht then you would suddenly become much more expensive on any Australian company’s P&L statement, and your position might be threatened by re-shoring.

In other words, in many of the environments where the Australian economy and AUD are strong, you are likely to benefit as this carries through into positive career development opportunities as well. However, with AUD as a barometer of global economic activity, a weakening currency may well signal the opposite. That is before even looking at cross-currency liability and debt situations (e.g. Aussie properties with Yen mortgages which have been a great idea for the last six months but which would look a lot worse if the AUD were the currently going rapidly into reverse).

On the flip side, in the face of a weakening AUD, international assets will start to look more attractive, which could be a much needed positive factor offsetting the drawbacks set out above – so there is a strong argument that maintaining a largely offshore foreign currency allocation provides inherent diversification benefits from an overall wealth standpoint.

With that in mind, it is also important not to over-react to short-term movements. While much media attention is dominated by the daily zigs and zags of currency volatility, our focus on underlying fundamentals has been the key to capturing the big moves over time and adding significantly to client returns.

It is common knowledge that China’s construction boom has been the driving force behind Australian mineral exports. As the chart shows, export commodity prices have become the dominant driver of the Australian Dollar, and have led to its doubling in value since 2001. However, while mineral prices have been the Australian economy’s key strength, they are also its key weakness, as China moves down an inevitable path of rebalancing away from physical investment and towards the consumer sector.

Australia’s “two-speed economy”, with growth outside the resource sector having been weak for some time, makes the country particularly vulnerable to a slow-down in exports. Along with a reliance on international funding to support the richly-priced housing market, this raises the prospect of further cuts to the Reserve Bank of Australia (RBA) cash rate and of stimulatory Australian government and central bank responses both of which would put additional pressure on the AUD.

Regardless of how long the AUD stays at these levels, we remain of the view that it is precariously placed if economic data should disappoint, and possibly with some catch-up due from the commodity price declines that we have already seen. As the US Dollar is still seen as the “safe-haven” currency of choice, minimizing holdings in AUD continues to be a good choice for Australian investors from a diversification standpoint. All this comes with the USD likely to rise in value at just the time that commodities and the AUD are sinking. Property prices will come under pressure and careers may take some unexpected turns.

The risks of an AUD downturn can be easily hedged against and the opportunities easily exploited. If you know what you are doing there is the chance to make some serious gains in your portfolio – even if Australia does look as though it will be going through a bad period. It is tantamount to bad risk management not to take advantage of this opportunity!

| The above data and research was compiled from sources believed to be reliable. However, neither MBMG International Ltd nor its officers can accept any liability for any errors or omissions in the above article nor bear any responsibility for any losses achieved as a result of any actions taken or not taken as a consequence of reading the above article. For more information please contact Graham Macdonald on [email protected] |

{kind=link}