As I was preparing a speech I recently gave at a Dataconsult breakfast (entitled Brexit Fall-out: the consequences of the UK referendum on EU membership for the parties concerned, for Asia and for Thailand), press reports showed that there was an unmistakable sense, in the post-referendum pandemonium, of the gradual dissipation of sheer panic. Among all participants.

Now former Prime Minister David Cameron and his lamentable Chancer of the Exchequer George Osborne were so cocksure that their wild and desperate punt would pay off that their only plan B consisted entirely of throwing their hands in the air, admitting that they wouldn’t have signed up for this governing malarkey if they’d known it was all going to become so hard and consequently passing the job to someone with even more vaunted ambition (hard to find) and greater willingness to roll their sleeves up (not so hard to find)1.

Labour leader Jeremy Corbyn, on the other hand, seemed so certain that there would be a narrow Remain referendum victory which would be so deeply unpopular with enough of the electorate that victory in the 2020 General Election was a certainty, he didn’t even bother with a plan B. It’s still somewhat surprising that Cameron feels able to question Corbyn’s leadership without himself feeling a significant hue of embarrassment about his own abandonment of leadership of state2.

The motley crew of Johnson, Gove and Farage who, for all the wrong reasons, led the campaign for Exit seemed so stunned by the outcome that the subsequent implosions of the latter two are testimony to the fact that they probably never even had a plan A, whereas Boris’ re-incarnation as Foreign Secretary is widely seen as a cunning plan by new PM Theresa May to give him sufficient rope to hang himself.

All of this could so easily have been avoided. Cameron and Osborne could have taken a leaf from the Irish (and Greek and French and Dutch) Government’s playbook – if a referendum looks close to call then have a ready-made rejection of the ballot ready or even cancel holding it altogether in trEU democratic style3.

Corbyn’s playbook was even easier. Some 41 years ago, the UK’s last great Labour PM, Harold Wilson, showed how to throw government and party behind one side (again Remain) but remain so personally aloof as not to be damaged by either outcome. In doing so he kept roaring giant lions like Anthony Wedgwood Benn firmly onside whereas Corbyn couldn’t even control whelping little pup Hilary Benn4.

All the 3 Brexiteers had to do was present the case honestly as to why the UK needs to exit the EU right now and the consequences of not doing so. Their combined inability to present any case credibly, let alone honestly, resembled the slapstick Three Stooges much more than the cunning 3 witches from Macbeth5.

Where does that leave us now?

Well in many ways in a much better place.

The fallacies of Osborne’s appalling economic policies of the last 6 years have been repeatedly highlighted by leading academics such as Professor David Blanchflower6 and my colleagues at IDEA Economics, Professor Steve Keen7 and Ann Pettifor8 amongst innumerable others.

Therefore, to save time and space, I won’t restate what has already been stated better than I ever could hope to. The best thing that can be said for Osborne is that he utterly failed to execute his dismal goal of balancing the UK national budget. Had he done so, the added appropriation of private assets and income streams by the government would have been even more socially calamitous and far worse than was seen in the 1920s and 1930s. The Jarrow Marchers would have seemed like Sunday afternoon picnickers. Fortunately, like many ideologues, his only saving grace may be that he wasn’t able to deliver more than a mere fraction of what he’d promised and now we’re saved from his particular brand of Old Etonian Riot Club idiocy – although sadly that doesn’t unfortunately preclude others, from different backgrounds, from trying to emulate it.

A new Chancellor can try to sweep the mess left behind away with a new broom – although I suspect the sweeping may be more akin to the famous Yorkshire cricket tail-end batting collapse in which the last man out (for a golden duck) blamed the situation that his predecessor (also out for a golden duck) had left behind9. But at least having someone else to blame can be liberating and enable a new course to be plotted.

However, just because politicians have been given an opportunity to the right things doesn’t mean that they’ll grasp it. In fact, it usually means the opposite which is why our base case is that the UK is likely to continue some, probably modified to make it mildly less unpalatable, version of the appalling Osbognomics policies that have pushed the UK economy to the very edge, although Professor Blanchflower is more optimistic about that, declaring austerity dead.10

Assuming that Article 50 (which has now come to resemble the Loch Ness Monster in that everyone’s heard of it but few, if any, have ever seen it) does get implemented – or at least that there is a long drawn out period of uncertainty while politicians kick it around with all the skill and teamwork of the England football team – then the biggest changes to the UK economy are likely to come from the currency effects of a weaker Sterling. Given the lengths that Japan, Europe and the rest of NIRP-land have had to resort in order to weaken their own currencies to competitive levels, then the mere act of getting 36 million UK registered voters to express their disdain for the EU looks extremely efficient in comparison.

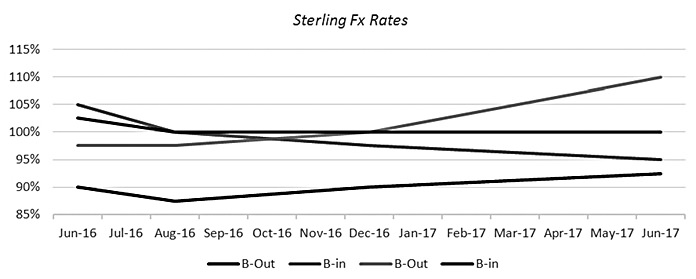

That said, Sterling weakness per se might be relatively short-lived. I’d continue to expect stabilization versus the Euro and against the riskier higher yield currencies (such as AUD and CAD within the next few months) although US Dollar strength in an uncertain global environment could be more enduring.

I produced some expectations prior to the Referendum of where I thought the Pound might head and these are re-produced on this page with only very minor updates (partly down to laziness but also due to the fact that these have so far been pretty well borne out by events and therefore I don’t see any great need to make too many sweeping changes – see chart).

In Part Two, I’ll take a look at equity markets and the global economy.

Footnotes:

1 “Why should I do all the hard shit for someone else, just to hand it over to them on a plate?”- David Cameron – http://www.huffingtonpost.co.uk/2016/06/25/the-waugh-zone-june-25-20_0_n_10668590.html

http://english.eu.dk/en/faq/faq/referendums

5 https://www.theguardian.com/tv-and-radio/2016/jun/27/john-oliver-brexit-vote-hbo-last-week-tonight

8 https://www.youtube.com/watch?v=2csPya47wik

9 ‘at Northampton in 1954 Johnny Wardle was bowled, horribly, by Tyson for nought. “A bloody fine shot that were,” snorted Trueman, as he went out, just before meeting a similar fate. “And a bloody fine shot that were, an’ all,” was Wardle’s greeting to Fred. But Trueman had a knack of getting in the last word: “Aye, I slipped on that pile o’ shit you left in the crease.” – http://www.espncricinfo.com/wisdenalmanack/content/story/292041.html

| Please Note: While every effort has been made to ensure that the information contained herein is correct, MBMG Group cannot be held responsible for any errors that may occur. The views of the contributors may not necessarily reflect the house view of MBMG Group. Views and opinions expressed herein may change with market conditions and should not be used in isolation. MBMG Group is an advisory firm that assists expatriates and locals within the South East Asia Region with services ranging from Investment Advisory, Personal Advisory, Tax Advisory, Corporate Advisory, Insurance Services, Accounting & Auditing Services, Legal Services, Estate Planning and Property Solutions. For more information: Tel: +66 2665 2536; e-mail: [email protected]; Linkedin: MBMG Group; Twitter: @MBMGIntl; Facebook: /MBMGGroup |

{kind=link}