When asked what the stock market would do, J.P. Morgan – founder of the eponymous investment bank – famously said, “It will fluctuate.”1 He is also widely attributed as commenting “The market will go up and it will go down, but not necessarily in that order.”2

Over a century after his death, those quotes couldn’t be any truer today: for the last few months, I’ve been saying that 2016 looks more unpredictable than any year I can ever remember. That’s why, for the first time in my career, I decided to hold back from an annual forecast and instead make provisions for the worst case scenario.3

What does ‘making provisions’ actually mean? If you ask Royal Bank of Scotland analyst Andrew Roberts, it means sell “everything except high-quality bonds.”4

However, there are better options: for example, having a portfolio with diversified asset allocation.5 This eliminates the temptation to rely too heavily on one type of asset. So if an investor has, say 40% of their portfolio in shares in companies within the same industry, any bad news in that sector could greatly reduce the portfolio’s value.

That sounds logical, but this principle doesn’t just hold for individual shares. When investing at asset class level – be it stock exchange indices, commodities, currencies, bonds etc. – it’s important to ensure your investments are diversified.

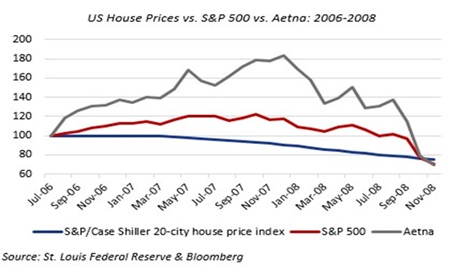

Sounds easy, right? Well it may not be. History has shown us how a drop in value of one asset class can adversely affect market confidence and thus influence the value of others. The 2008-2009 global financial crisis is a case in point. One of its many triggers was the over-mortgaging and subsequent bubble-burst in US house prices. If you’d owned shares in the long-time S&P 500 healthcare company Aetna at the time, you would have thought that there was little relation. Yet, Aetna’s price followed the trend of the overall S&P 500 and went south as house prices started to drop (see chart 1).

Chart 1

Chart 1

Of course you could argue that practically every investment, irrespective of sector or geography, is affected by major events, such as the global financial crisis. You may also point out that placing money somewhere which is almost totally risk-free, such as a bank account, will bring scant return.

What every investor needs to do, you could argue, is buy low and sell high. In most years, I would say doing this with individual stocks is more random than rolling a dice. It’s all about the timing, which is something not even the most lauded experts can predict – take the performance of Warren Buffet’s Berkshire Hathaway for example (see chart 2).

Chart 2

Chart 2

So what is really needed in these uncertain times is some form of insurance policy: something which can counteract against the volatility of the markets.

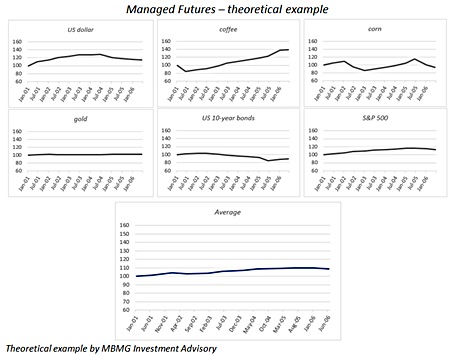

One option is a managed futures fund. That may sound like some form of high-risk hedge fund we read about in the press.6 However, a sensibly-managed fund as part of a portfolio can take advantage of the markets’ ups and downs. By sensible, I mean using true diversification. One fund manager I spoke to recently showed how a fund he uses tracks scores of futures markets, such as stock market indices; commodities like crude oil, gold, soybeans, milk, currencies; and bonds. The markets’ prices are analysed to see how similar their behaviour is to each other – only markets with sufficiently distinct price movements are chosen for the fund. This strategy is to ensure that in most scenarios, there is always one asset bringing in some form of return. As such a fund comprises of futures, it can gain in value whether the price goes up or down – the crucial factor is that there is a defined trend that a fund manager can follow shortly after the trend is underway.

Chart 3

Chart 3

Most trend-following or managed futures rely on some degree of systematic pattern recognition rather than relying on gut feeling or attention to company news, media reports, weather forecasts or any other type of opinion-based prediction – just analytics based on past trends.

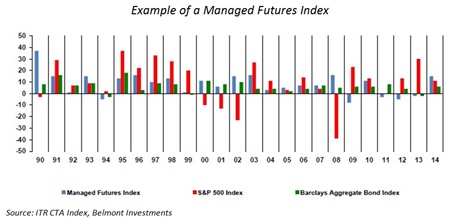

With all this in mind, it may be tempting to put your whole portfolio into managed futures with the objective of making a reasonable – if not spectacular – return. However, there are three main flaws to this strategy: you would become totally reliant on the short/long activity of a single strategy; such funds tend to do well when there are clear trends but don’t perform when there is a plateau in prices, as it’s difficult to see where in which movement the next direction will be; and managed futures can largely underperform when stock markets, bonds or other assets are increasing in value (see the 25 year chart below) but perform very positively when such markets fall sharply.

25 year chart

25 year chart

The old saying “stock markets go up in escalators but come down in elevators,” still has some truth to it.

Consequently, managed futures represent a useful insurance policy within a diversified portfolio. It represents an interesting example of how you can balance out a portfolio, so that you’re not totally exposed to whatever bad news the markets may bring. Even though by itself it can be quite a volatile asset class, much of that volatility is inverse in direction to traditional assets like stocks or bonds – therefore blending these can actually reduce volatility while also increasing return.

So we can insure ourselves against J.P. Morgan’s fluctuations. Although they didn’t have managed futures or trend following 150 years ago, even Morgan himself didn’t leave everything to chance. During the American Civil War, he used to cable outcomes of battles – prior to their general knowledge – to the London office of his father’s firm. That actually did enable the firm to buy US war bonds low and sell them high7 although these days he’d almost certainly find himself in trouble for ‘market timing’.

Footnotes:

1 Middletown Times Herald (Newspaper) – February 28, 1934,

2 https://www.aaii.com/programs/conference/presentations/Mirsky_Risk% 20101-How%20Much%20 Risk%20Is %20in%20Your% 20Portfolio.pdf

3 http://www.mbmg-investment .com/in-the-media/inthemedia/75

4 idem

5 http://www.investopedia .com/articles/02/111502.asp

6 http://www.pionline.com/article/20160502/PRINT/160509986/public-pension-funds-feeling-the-heat-in-hedge-fund-furor

7 Chernow, Ron (1991), The House of Morgan: An American Banking Dynasty and the Rise of Modern Finance, New York: Grove Press

| Please Note: While every effort has been made to ensure that the information contained herein is correct, MBMG Group cannot be held responsible for any errors that may occur. The views of the contributors may not necessarily reflect the house view of MBMG Group. Views and opinions expressed herein may change with market conditions and should not be used in isolation. MBMG Group is an advisory firm that assists expatriates and locals within the South East Asia Region with services ranging from Investment Advisory, Personal Advisory, Tax Advisory, Corporate Advisory, Insurance Services, Accounting & Auditing Services, Legal Services, Estate Planning and Property Solutions. For more information: Tel: +66 2665 2536; e-mail: [email protected]; Linkedin: MBMG Group; Twitter: @MBMGIntl; Facebook: /MBMGGroup |

{kind=link}