We have battened down the hatches from a tactical asset allocation perspective over the past few weeks. In a crisis, we have learnt that if you need to panic, it is best to have panicked first! Those asset allocators who have issued statements over the last few weeks that they are sitting out this volatility are generally overweight global equity and do not have much choice. But are we nearing the end of the secular bear market in developed world equities?

BCA Research, well regarded independent researchers since 1949, wrote a special report on this topic recently that we think summarizes all the key current strategic asset allocation issues:

Global Developed Market (DM) Equity

1. When one formulates an investment horizon for a strategic benchmark over a decade, raise neutral developed world weightings.

2. Stay neutral at a cyclical level relative to the above benchmark.

3. Adjust weightings in response to policy developments.

It is obvious that after twelve years of a bear market in DM equity, valuations are much better value; they are also cheap versus government bond yields in the US and Europe. However, BCA added the following points:

* The “Greenspan put” on the equity market has become the “Bernanke call” on the bond market.

* There is an opportunity to increase neutral strategic equity positions on weakness. Over the next decade, real returns could well begin to revert toward the average real compound returns of the last 100 years, or even better and the amazing returns of the 1950s, early 1960s, 1980s and 1990s.

* However, the smooth transition from a secular bull market in bonds to one in equities is seldom smooth. Historically, in the first year following a bond market secular reversal, equity markets have tended to decline. An involuntary US fiscal tightening in 2013 may prompt history to repeat itself.

* Aggressive cyclical allocation around a higher benchmark position will, therefore, be required. It will be next to impossible to anticipate the whims of policy makers.

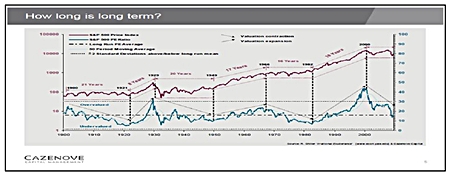

The chart from Cazenove (which we have shown many times over the years) explains why strategic DM equity weightings should be increased but can remain volatile for some time to come.

In conclusion, in January we increased our strategic long term weightings to DM equity in global accounts and funds as part of a gradual process. But we do not blindly follow value or mean reversion, as short term tactical asset allocation is required to manage volatility. Finally, in our opinion, the European Central Bank not lending to insolvent banks from mid-May is a policy development that required an adjustment in weightings!

| The above data and research was compiled from sources believed to be reliable. However, neither MBMG International Ltd nor its officers can accept any liability for any errors or omissions in the above article nor bear any responsibility for any losses achieved as a result of any actions taken or not taken as a consequence of reading the above article. For more information please contact Graham Macdonald on [email protected] |

{kind=link}