Recently, China’s central bank, the People’s Bank of China (PBOC), reduced its reserve-requirement ratio (RRR) by a record-equalling 1% (or 100 base points).

RRR is the percentage of depositors’ balances a bank must retain in cash – the rate is usually set by the central bank. The reduction of this amount is an easing tool, designed to encourage banks to lend more and reduce interest rates.1

The PBOC’s action comes just days after an official announcement that in Q1 2015, Chinese economic growth was the slowest in six years.2 Chinese officials suggested that areas such as industrial output and retail sales caused concern.3

The PBOC had previously implemented steps to stimulate lending, such as the medium-term lending facility. Despite its name, this is a short-term credit programme which made RMB 370 billion (USD 59.6 bn) available in Q1 2015, according to the central bank.4

A desperate measure

The new RRR of 18.5% may still be high by global standards5 but the fact that this is the second cut in just 2 ½ months and the joint biggest ever single reduction (the other was in 2008) smacks of desperation. The move is designed to release RMB 1.2 trillion (USD 194 bn) of liquidity,6 in order to halt the economic slowdown. While official figures put economic growth at the targeted 7% level, I have my doubts that it was really that high.

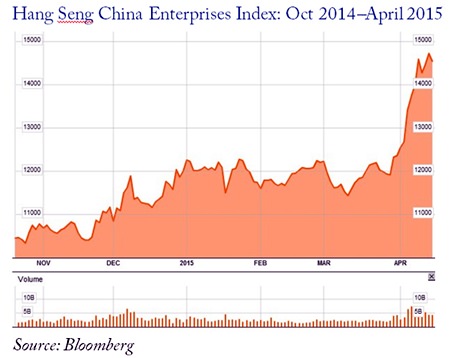

The reality is that the Chinese economy is weak and the equity markets are strong; although comparing the volume of shares traded on the Shanghai Composite to that on the Hang Seng China Enterprises Index shows that most of the recent trading in Chinese companies’ equity is being done in Hong Kong.

This emphasizes the scale of gross and net outflows, now that exports have dried up.7

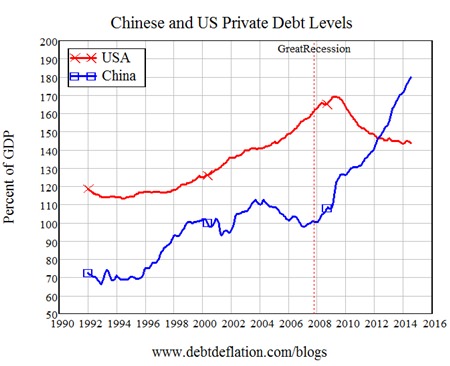

The fact is that China is currently dealing with many economic issues. It has bloated housing and construction sectors which are consequently suffering.8 Not only that, it is facing a private debt time-bomb, similar in scale to that seen in the US sub-prime market in 2007.

Of course, the main difference between the two scenarios is that the US government was guilty of dereliction of duty in 2007. Today the Chinese government is actually the main cheerleader of private debt9 – especially since it moved the sector itself as a developer to support the market – and playmaker.

With that in mind, my view is that more liquidity is not what is needed – all that will do is simply shore up debt and mal-investment problems. Contacts in Hong Kong tell me they believe that the Chinese money flowing into Hong Kong-listed stocks right now10 is a sign of distrust in the government and the mainland’s financial institutions.

The effects on the Chinese economy

It’ll be interesting to see how people will react to the PBOC’s RRR announcement. Will people find a workaround? Will this redress the lack of confidence? I don’t think so: once the exuberance dies down, I think it will undermine the economy further.

Will this cure China’s underlying debt problems? Not in my view. In fact, I think it will make them worse. As for helping the economy as a whole: I think the restriction change will ultimately stifle it.

One effect the change may have is to boost the property market; however, this may be in the very short term, putting air into a bubble that is trying to deflate. With that comes the risk of bursting that bubble.

Even though the first full trading day since the announcement saw falls in the Shanghai composite and the Hang Seng,11 I do think the RRR change will boost stock prices in Mainland China. However, Hong Kong will probably trade most of this – thus defeating the aim of stemming capital outflows. Should Hong Kong prices go up in the short run, it would mean the PBOC will have to pull another rabbit out of the hat to avoid a fall-back.

In essence, the PBOC is using the wrong tool for the wrong job. It has tried to address this by cutting the RRR by 200 base points for rural credit co-operatives and 300 base points for the China Agricultural Development Bank.

Any way I look at these RRR cuts, they strike me as desperate moves. Not only that, the PBOC is replicating the flawed policies of pushing on a string, implemented by Western governments in 2008. Those policies have left many countries facing a deflation crisis, worryingly similar to that experienced by Japan over the last quarter-century.

Footnotes:

1 http://www.frbsf.org/education/publications/

doctor-econ/2001/august/reserve-requirements-ratio

2 www.reuters.com/article/2015/04/15/us-china-

economy-gdp-idUSKBN0N52E220150415

3 Xinhua news agency

4 http://www.bloomberg.com/news/articles/2015-04-19/

china-follows-on-stimulus-pledge-with-bank-reserve-ratio-cut

5 idem

6 idem

7 idem

8 http://www.dw.de/chinas-real-estate-market-

weighed-down-by-oversupply/a-18207416

9 http://www.ideaeconomics.org/blog/2015/1/13/

steve-keens-2015-outlook

10 http://www.ft.com/intl/fastft/306563/hk-shares

-7.5-yr-high-mainland-chinese-buy

11 http://www.reuters.com/finance/markets/asia

| Please Note: While every effort has been made to ensure that the information contained herein is correct, MBMG Group cannot be held responsible for any errors that may occur. The views of the contributors may not necessarily reflect the house view of MBMG Group. Views and opinions expressed herein may change with market conditions and should not be used in isolation. MBMG Group is an advisory firm that assists expatriates and locals within the South East Asia Region with services ranging from Investment Advisory, Personal Advisory, Tax Advisory, Corporate Advisory, Insurance Services, Accounting & Auditing Services, Legal Services, Estate Planning and Property Solutions. For more information: Tel: +66 2665 2536; e-mail: [email protected]; Linkedin: MBMG Group; Twitter: @MBMGIntl; Facebook:/MBMGGroup |

{kind=link}