Whilst the news headlines have been occupied by Greece, Ireland, Spain and the US fiscal cliff, it is interesting to investigate investment growth opportunities as uncorrelated from the Western world as possible.

Not a day goes by where large US or UK multinationals or South African corporations are announcing capital expansion, acquisitions or organic growth plans for Africa. Institutions are now following the great retailers and private equity frontier raiders into the continent. It was the recent announcement that the SAR150 billion Government Employees Pension Fund, Africa’s largest retirement fund, is considering investing around 5-15% of its portfolio in Africa (ex-South Africa) to gain access to superior growth prospects.

Source: African Economic Outlook, June 2012

Without stating a blinding glimpse of the obvious in frontier markets, Sven Richter from Renaissance Asset Managers says: “The people who are in Africa first will see a tremendous benefit as the people who come in second push up the prices.”

Let’s look at Africa for a moment. Africa contributes less than 2% to global GDP despite being 14% of the World’s population and having one fifth of the world’s landmass. The continent is well positioned for long term sustainable growth given its abundance of resources, land and cheap labour. Political risk in Africa has dramatically declined in many of the continent’s nations and this sets the stage further for long term sustainable growth. The number of countries which have been under military rule or one-party states has dropped from 76% in 1982 to 10% today and debt to GDP has been reduced from 70% in the ’90s to 20% today. GDP growth is expected to be significantly higher than the global average for the foreseeable future.

Source: African Economic Outlook, June 2012

Foreign investors are heavily underinvested in African markets, with the exception of South Africa and Egypt. There are twenty-three stock exchanges in Africa ranging from start-ups like Rwanda to the more established ones like those of Egypt (1888) and Johannesburg Securities Exchange (1887). Despite all the potential, the amazing thing is that African combined market capitalization adds up to only 1% of world market capitalization.

Investing in Africa adds diversification to the global investor’s portfolio. Africa represents the last truly emerging continent in the world and should be part of any long term investor’s portfolio.

Goldman Sachs produced a report last year which stated that the 10 most populous countries on the African continent could grow their economies to almost USD17 trillion by 2050. Whilst South Africa, Egypt and Nigeria have the largest absolute growth potential, Goldman Sachs noted that Tanzania and Uganda also had the potential to have economies 50 and 43 times larger by 2050 respectively. The most interesting point from the report was that whilst the BRIC’s (Brazil, Russia, India, China) growth rate is expected to fall from an average of 8% in the 2011-10 period to 3.5% average in 2041-2050, Africa is expected to continue to increase from the current 6% average in the current decade to 7.5% in 2050.

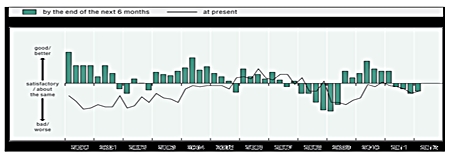

Twenty-two African countries are ranked in the top 50 countries according to projected real GDP growth 2011/12 from the IMF. A sample includes Angola 5.8%, Nigeria 6.0%, Egypt 6.5%, Mali 5.0%, Zambia 7.3% and Cameroon 4.5%.

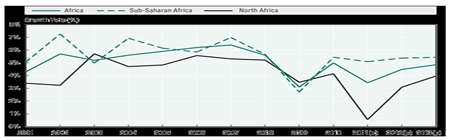

According to the African Economic Outlook in the chart below, African GDP growth as a whole fell in 2009, along with the rest of the world, from 6% to 3% but has now recovered. The correlation and reliance on resources and commodities can be seen with the slowdown last year. The political uprisings in North Africa, surprisingly, have not derailed the train and an aggressive bounce is forecast in Egypt et al for this and next year.

However, growth is one thing and valuation and liquidity of investments are another. Whilst Africa offers the largest growth outside Asia and a larger growing middle class than India, 45% of the population is under 15 and with increased consumption and infrastructure spending it will probably remain an enigma, therefore requiring significantly more analysis. Nonetheless, for the long term, it should be a small part of anyone’s aggressive portfolio BUT please remember to remain liquid just in case something catastrophic happens – this should apply to all of your portfolio.

| The above data and research was compiled from sources believed to be reliable. However, neither MBMG International Ltd nor its officers can accept any liability for any errors or omissions in the above article nor bear any responsibility for any losses achieved as a result of any actions taken or not taken as a consequence of reading the above article. For more information please contact Graham Macdonald on [email protected] |

{kind=link}