PATTAYA, Thailand – Thailand’s economy has emerged from what officials describe as its most dangerous phase, with growth momentum returning faster than expected and optimism building for a stronger expansion in 2026.

Deputy Prime Minister and Finance Minister Ekniti Nitithanprapas said the economy has “climbed out of the abyss” following a sharper-than-forecast rebound in late 2025, expressing confidence that GDP growth in 2026 could exceed 3 percent as investment accelerates.

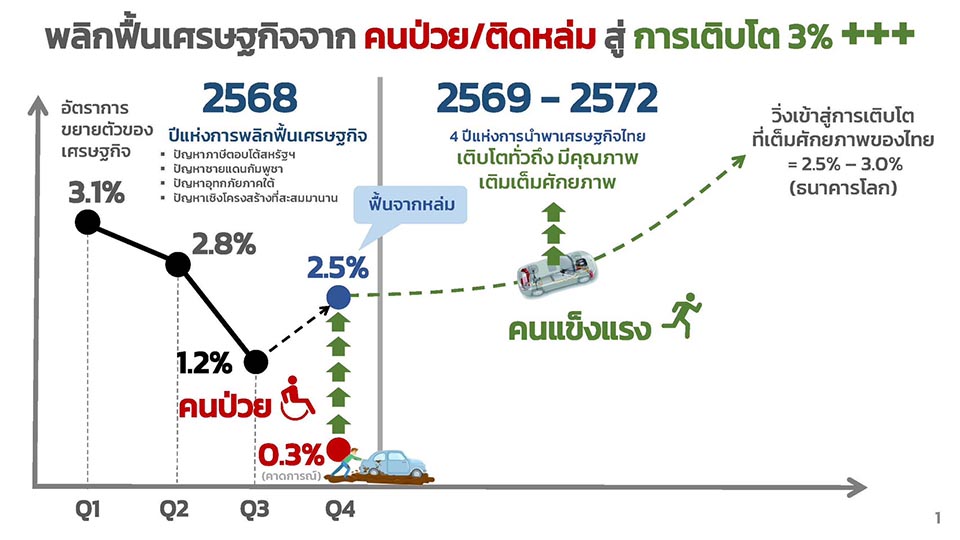

The upbeat assessment followed the release of fourth-quarter 2025 figures by the National Economic and Social Development Council, which showed the economy expanding 2.5 percent year-on-year—far above earlier projections of just 0.3 percent. Full-year growth came in at 2.4 percent, defying fears that Thailand was heading into a prolonged economic slump.

Mr. Ekniti credited a series of late-year stimulus measures, including expanded co-payment schemes, domestic tourism incentives, and faster disbursement of government training and seminar budgets. These steps helped lift consumer confidence, investment sentiment, and stock market performance, allowing liquidity to spread across regional economies nationwide. As a result, Thailand’s economic output reached an estimated 19 trillion baht—around 300 billion baht higher than initially forecast.

Private consumption grew 3.3 percent, accelerating from an average of 2.5 percent seen in the first three quarters of the year. Even more striking was the surge in investment: total investment expanded by 8 percent, driven by a 15 percent jump in private sector investment and a 6 percent rise in public investment—well above earlier growth of just 2–3 percent.

Calling the figures a “clear signal of renewed confidence,” Mr. Ekniti said the government is preparing to push legal and regulatory reforms to further unlock investment, including fast-tracking approvals through the BOI Fastpass initiative. The proposal will be submitted to Deputy Prime Minister Borwornsak Uwanno as part of broader efforts to make Thailand a more competitive investment destination.

He added that fiscal discipline remains a cornerstone of government policy, a factor that recently led S&P Global Ratings to reaffirm Thailand’s credit outlook as “stable.”

Looking ahead, the Finance Ministry expects economic growth in 2026 to exceed 3 percent. “The patient has left the ICU and is learning to run again,” Mr. Ekniti said. “Now the task is to ensure growth is efficient, inclusive, and sustainable—using budgets precisely, maintaining fiscal discipline, and keeping investment moving.”

The government has branded 2026 as the “Year of Investment,” aiming to restart private-sector engines through regulatory unlocks and consistent policy execution. If momentum is sustained, officials believe Thailand’s economy can finally shift from recovery mode to full-potential growth. (TNA)

{kind=link}